I think everyone has heard the term “life insurance”. But if you were asked to tell someone about life insurance, would you, do it? What if you need to describe different terms, conditions, or types of insurance? What is life insurance for? How long is it guaranteed? Who needs it? It may seem complicated, but the answer is quite simple.

The original role of life insurance was to provide your loved ones with a tax-free amount of money after your death, allowing them to continue to achieve their financial goals.

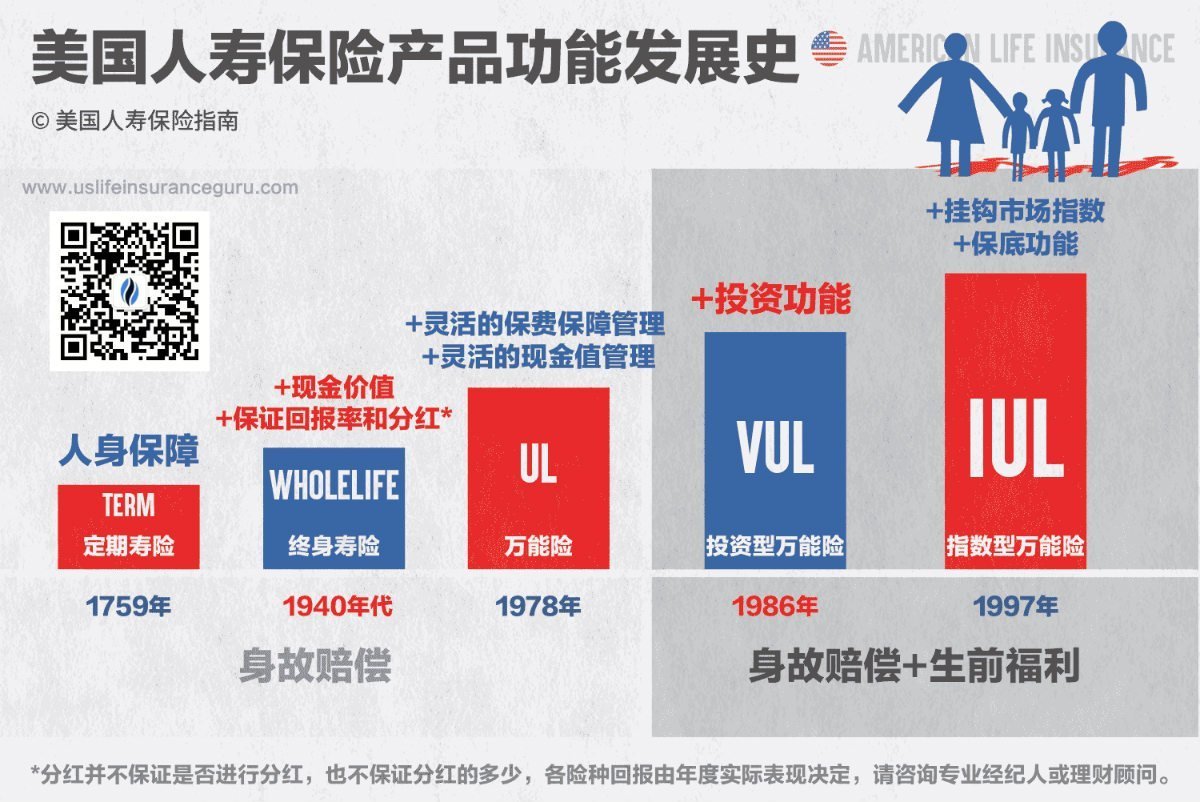

Until now, the lifetime cash value life insurance policy in the United States has evolved into a sophisticated and professional comprehensive financial product that is used to meet various needs such as sickness, taxation, inheritance, and wealth.

In the U.S. Life Insurance Guide, you’ll learn:

- What is life insurance?

- How Life Insurance Works

- Benefits of Life Insurance

- Why is life insurance important?

What is life insurance?

Life insurance is a contract between the policyholder and the insurer (company) or insurer, under which the insurer (company) undertakes to pay a penalty to the named beneficiary in the event of the death of the insured (usually the policyholder).

Life insurance is a legal contract, the terms of which describe the limits of the insured event. Common examples are lawsuits related to suicide, fraud, war, riots, and others.

How does life insurance work?

In the next step, we will learn how to understand the general components of a policy, how to apply for it, and the different types of policies and their associated fees.

What are the general characteristics of life insurance?

Regardless of the type of policy you buy, life insurance includes the following 5 parts:

Insured / Insured A living individual insured by a life insurance company.

Policyholder / Policyholder The person or institution that owns this life insurance policy.Generally, in the event of the death of the insured, a death benefit is paid.

Beneficiary/Beneficiary The person or institution receiving the payment.More than one beneficiary may be appointed.

Premium/Premium Payments are made monthly or annually to keep the policy in effect.

A life insurance policy takes effect as soon as you pay your first premium, which means that once the policy goes into effect, you are eligible for death benefits.

The insurance company is not obliged to pay death benefit in the following exceptional circumstances:

- The policyholder’s life insurance policy has expired

- The policy is out of date or canceled

- The death occurred within two years of the policy’s entry into force, and the insurer found evidence of fraud in the application.

How do I apply for life insurance?

Applying for life insurance from start to finish often takes 3 to 8 weeks, but you can usually complete the process in just 7 steps.

1. Get free plans and quotes.By comparing the plans and rates of different insurance companies, you can be sure that you will get the exact policy plan you need.

2. Choose your policy.Consider your goals, costs, customer service, and average application time.

3. Fill out the application form.You can fill out the application form online or get help from an authorized professional.

4. Take part in a medical examination. As part of the coverage process, you may be required to undergo a physical exam similar to a basic physical exam. After 2020, with the development of big data technology and technology, many insurance companies provide an insurance process without a medical examination, For healthy policyholders between the ages of 18 and 50, the policy can be issued no earlier than 5 days later.

5. End the interview. The insurance broker will ask you a few questions about lifestyle and health.

6. Wait for approval.The insurance company will collect all the information to determine the final premium, which should be similar to the price you received.

7. Sign your policy.Your policy will take effect after you sign the policy and pay your first premium.

For more information, find out exactly what to do when applying for life insurance.

What are the different types of life insurance?

“Life insurance” is just a general term specific to insurance products, there are many kinds of products.

{kind=link}

Life insurance for the term/term

Term life insurance is valid for a certain number of years, called term.When this period ends, the policy is declared expired.It is usually the most affordable type of life insurance that is used to provide the beneficiary with a death benefit for the number of years you need.

Life Insurance/Permanent

Full life insurance also has a cash value component as an investment tool that can be used.

Life insurance products include:

- Participation in life/whole life insurance

- Universal Insurance/Universal Life

- Investment Universal Insurance VUL/Variable Universal Life

- Guaranteed Universal Life

- IUL Indexed Universal Lifespan/Indexed Universal Life

Term life insurance vs life insurance in general

I believe that most users who are new to American life insurance will ask themselves this question. Term life insurance is a good option for most people as it is affordable and simple. A financial professional who can help you determine which option is best for your needs.

How much does life insurance cost?

The estimated cost of term life insurance with coverage of $20,250,000 for a 160-year-old non-smoker is about $XNUMX per year, according to LIMRA, the trade association of the American Association for Life Insurance Marketing and Research. Of course, the number of policies covered, the type of coverage, and the length of the coverage period will also affect the speed.

Different insurers weigh these factors differently, so it’s important to compare offers from multiple companies to make sure you’re getting the most affordable package.

What are the benefits of life insurance?

If you accept life insurance as part of a family protection plan, you have the following significant benefits.

Tax-free financing

The death benefit provided by a life insurance policy is a tax-free sum of money, which means that the entire amount will be transferred to your beneficiary in full.

It’s an affordable protection plan for everyone

Think about it: A healthy 30-year-old man can pay as little as $40 per month for a lifetime life insurance policy with $100,000 XNUMX coverage Mortgages, retirement planning, and even serious injuries and illnesses, it’s worth it.

This is another investment tool

Term life insurance is simple, but life insurance products with a cash value function can be used as a mandatory investment vehicle (as opposed to mandatory savings). If you already have other tax-free investment options (e.g., ROTH IRA, government bonds), life insurance products can be another additional investment for your financial instruments.

Why is life insurance important?

It is important to engage in family or personal financial planning, but if you are the main source of family income and you are dying, any planning is pointless.

- Future protection plans for your family, such as college plans and tax-free lifelong income plans after retirement.

- Pay off your mortgage or student loan

- Legacy and succession planning for children, grandchildren, or the community

- Pay for funerals and other end-of-life expenses, statistically, the average cost is around $10,000 XNUMX.

For more information, find out exactly what life insurance does and what it does.

Who needs life insurance?

Life insurance is a useful tool for most people, but that doesn’t mean everyone needs it.

- You have no beneficiaries.Over time, the later you buy, the more expensive your life insurance premiums are, so you should probably apply when you’re young, when your expenses are low. leaving money to some organizations or charities.

- You don’t have (or aren’t expected) to have any debt.But you should also consider future debts, such as the cost of sending your children to school or caring for aging parents.

- You can insure yourself.Even if you have or have debts, you can use your savings to pay them off in full.

If you don’t have one, you can cause financial damage to your loved one in the worst case, which can be easily avoided with life insurance.